In recent years, India has witnessed a remarkable transformation in its investment culture. Thanks to relatable campaigns like “Mutual Funds Sahi Hai”, millions of Indians who once kept savings idle are now exploring SIPs, equity funds, and other financial instruments. The success of this movement lies in one word: awareness.

Now, it's time to ask—if we could revolutionize investments with a simple slogan and smart education, why can’t we do the same for credit scores?

Because in many ways, “Credit Score Important Hai” might just be the next national campaign India desperately needs.

Why Credit Scores Matter (More Than You Think)

Most urban, salaried individuals might already be familiar with their credit score. But for a vast majority of India’s working population—especially in Tier 2 and Tier 3 cities—credit scores remain an unfamiliar concept, or worse, a misunderstood one.

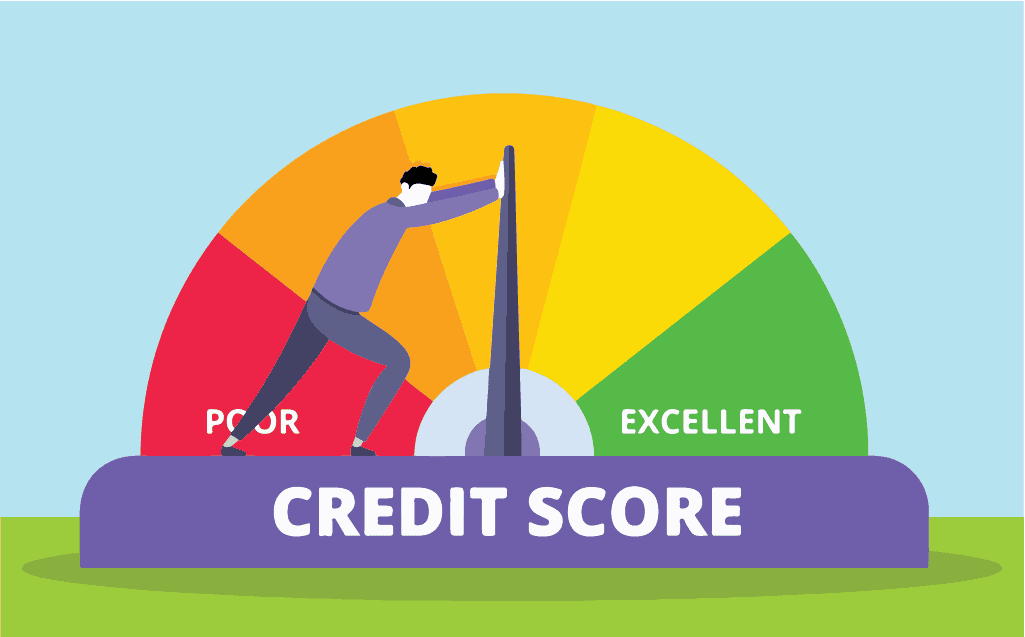

A credit score isn’t just a number. It’s a financial passport. It determines whether a person can get a home loan, a car loan, or even a smartphone on EMI. It decides the rate of interest they’ll pay, or whether they’ll be shut out of formal finance altogether.

But what happens when people don’t understand this?

They turn to moneylenders, pledge gold, or borrow informally—often at predatory rates. And this financial exclusion leads to a cycle of poor credit habits, missed repayments, and worsening credit health.

The Big Picture: Why This Hurts India’s Growth Story

For India to grow at 8%+ GDP consistently, domestic consumption must be a strong pillar. That means more people buying homes, vehicles, appliances, investing in education, and starting small businesses. And all of this hinges on access to credit.

Yet, large sections of the population remain underserved—not because credit isn't available, but because they lack the credit profile to access it.

And this gap isn't due to fraud or risk—it’s due to ignorance. People don’t realize that:

- A missed EMI on a ₹5,000 loan affects them for years.

- That holding multiple credit cards and maxing them out reduces their score.

- Or that paying just the minimum due doesn’t help their credit health.

Without intervention, this ignorance becomes systemic. It holds back financial inclusion, hinders entrepreneurship, and curtails consumption-led growth.

A Lender’s Perspective: What We See on the Ground

As a lending institution catering to India’s middle-income segment—the so-called “middle of the pyramid”—we see this play out daily.

- Customers with decent incomes are denied loans because of past defaults they didn’t even realize were hurting them.

- Others are shocked to learn they have a low credit score due to a forgotten utility bill or co-signed loan default.

- And many don’t know what a credit bureau is, let alone how to fix their score.

This isn’t just a personal financial problem—it’s a national one.

What Needs to Be Done: The 2-Point Plan

Just like “Mutual Fund Sahi Hai” democratized investing, we need a similar movement around credit awareness. Here’s how:

1. Launch a Nationwide Awareness Campaign

Let’s take the “Credit Score Important Hai” message to the masses—TV, radio, cinema halls, mobile apps, and even rural touchpoints like post offices and gram panchayats.

People should understand:

- What a credit score is.

- How it’s calculated.

- Why paying on time matters.

- How to check and improve their score—without middlemen or scams.

This isn’t just good economics—it’s nation-building. Financially aware citizens are more confident consumers, smarter borrowers, and more responsible investors.

2. Reward Good Credit Behavior

Imagine if maintaining a high credit score came with financial perks—not just cheaper loans, but direct incentives.

- A rebate on income tax for those with a score above 750.

- Lower insurance premiums.

- Special access to government-backed schemes or subsidies.

This would make creditworthiness aspirational. Just as people flaunt their CIBIL score on social media or brag about their salary hikes, they would begin to see good credit behavior as a point of pride.

Credit Discipline Is Culture

For this to succeed, it can’t just be a campaign—it has to become part of our culture. Just like we teach children to save, we must teach them to borrow responsibly. Credit score education must enter school textbooks, college seminars, and workplace onboarding.

Just like we made tax-saving investments a ritual, we need to make checking your credit score an annual habit.

And just like we normalized SIPs, we need to normalize conversations around EMIs, credit cards, and financial responsibility.

Government, Lenders, and Fintechs Must Work Together

This mission can't be left to one institution. It must be a coalition:

- Government ministries must lead awareness efforts, perhaps under the Financial Literacy umbrella.

- Banks and NBFCs must simplify credit reports and proactively educate consumers.

- Fintech apps should offer free score-checks and gamified credit coaching.

- Employers can partner to conduct credit awareness workshops as part of financial wellness programs.

The Time Is Now

India is at a financial inflection point. We’ve digitized payments, formalized banking, and opened the gates to investments. But credit discipline is still playing catch-up. Without fixing this, we’ll always be trying to push economic growth with one engine.

So, let’s say it loud and clear: Credit Score Important Hai.

Let’s educate, incentivize, and inspire.

Because a financially strong citizen is the foundation of a financially strong India.